The Mandate Most CEOs Misread

Private equity firms don’t just invest in companies, they invest in growth theses within those companies.

A growth thesis is a clear view of how the company will increase revenue and enterprise value over the hold period, supported by defined exit targets that track progress across each quarter (for example: expanding into a new segment, increasing deal size, improving retention, or driving more efficient pipeline generation).

Some CEOs misread the thesis as a suggestion. In practice, it is the yardstick investors use to evaluate performance and progress against exit targets.

The CEO’s role is to demonstrate that thesis can be executed on a defined timeline, with transparency and accountability to the board.

This changes how the CEO is evaluated. The focus shifts quickly from planning and positioning to demonstrating progress against the growth thesis. As timelines compress under private equity ownership, commercial execution becomes one of the highest-leverage areas the CEO directly influences.

In the first 100 days, many PE-backed CEOs encounter challenges in three areas:

Over-delegating commercial strategy to the CRO

The CEO assumes the CRO will build the go-to-market plan. The CRO optimizes within their function, but the connection between execution and the investment thesis is not always explicitly defined. This can lead to misalignment in how progress is communicated to the board.

Getting pulled into tactical execution

The CEO spends significant time in pipeline reviews and deal strategy, instead of focusing on the core decisions that determine how the business scales.

Operating with a founder-style approach

The CEO relies on intuition, delays prioritization, or builds execution plans that may not reflect the level of structure and rigor expected by investors.

This article outlines a structured approach to sequencing decisions, aligning teams, and executing within the first 100 days.

What should a PE-backed SaaS CEO focus on in the first 100 days post-investment?

In the first 100 days, a PE-backed SaaS CEO should focus on four sequential growth decisions and align the business to the investment thesis through a defined execution plan.

The four core decisions (Push Order of Operations):

- ICP Decision — who to target

- SLA Decision — how those targets convert

- Contribution Decision — where bookings come from

- OKR Decision — what the CEO prioritizes long-term

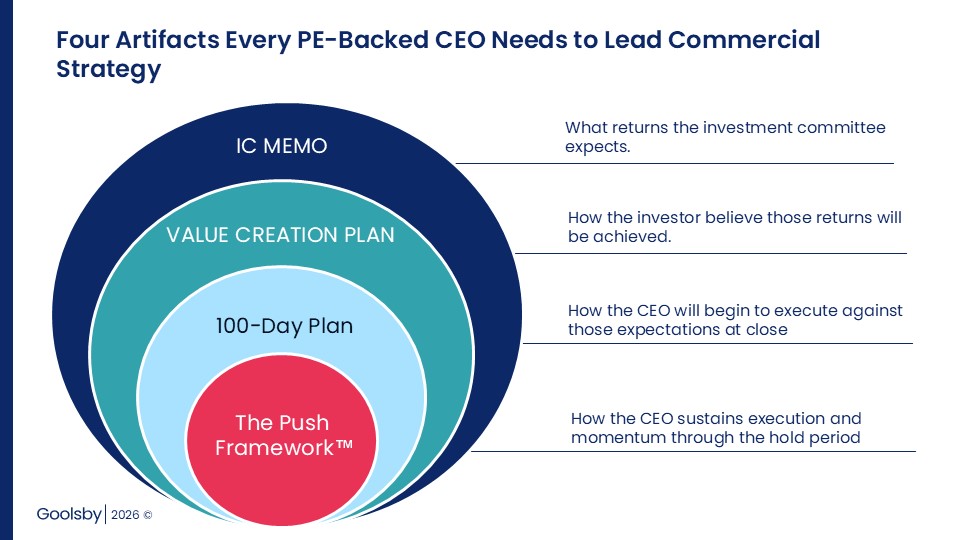

Before the first board meeting, the CEO should review four key artifacts:

- IC Memo — investor expectations

- Value Creation Plan — growth levers

- 100-Day Plan — execution sequencing

- The Push Framework — system for sustained execution

The sequencing matters because each decision and artifact builds on the previous one, creating a coordinated approach to commercial execution.

Four Artifacts Before the First Board Meeting

Before presenting to the board for the first time, it is important to have reviewed and understood four core documents. These artifacts provide context on what the investor acquired, why the investment was made, and how execution is expected to unfold.

Artifact 1: The IC Memo

The Investment Committee Memo is the document used to approve the deal. It outlines the thesis: why this company, at this valuation, with this growth trajectory, is expected to deliver the target return.

The CEO’s role is to understand and translate this thesis into terms the leadership team can execute against. The IC Memo provides a clear view of investor expectations, which informs downstream decisions.

Artifact 2: The Value Creation Plan

The Value Creation Plan connects the investment thesis to operational levers. It defines the milestones expected during the hold period to support enterprise value creation and exit outcomes.

The level of detail can vary by firm. Some provide a fully developed plan, others may provide a high-level outline, some may expect the CEO to develop it. In any case, aligning on a clear Value Creation Plan is important, as it serves as the anchor for execution.

Artifact 3: The 100-Day Plan

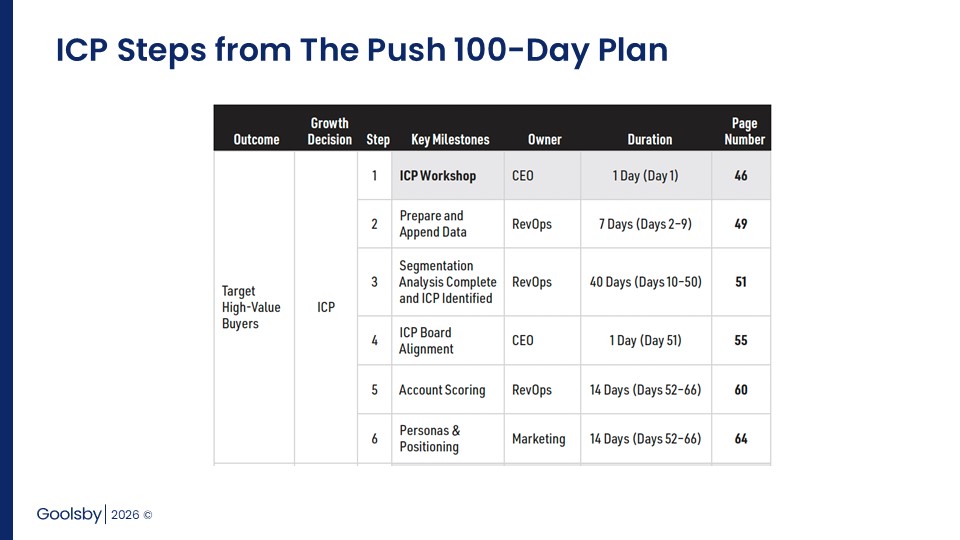

The 100-Day Plan sequences the initial phase of commercial execution following the investment. It is not simply a list of initiatives, but a structured sequence of activities with defined milestones, owners, durations, and dependencies. The goal is to coordinate execution and reduce risk during a period when significant capital is being deployed.

In the Push Framework, the 100-Day Plan is designed as a full build of the commercial system and includes all 17 execution steps across four growth decisions, beginning with the ICP Workshop and concluding with enablement milestones. This plan becomes a central operating tool for the leadership team.

Artifact 4: The Push Framework

The Push Order of Operations Framework defines how growth decisions are made and operationalized going forward. It guides teams through the four core growth decisions required for scale (ICP, SLA, Contribution, OKRs) and sequences them so that each creates the inputs for the next. This sequencing creates interlocks across functions, aligning execution across Sales, Marketing, Customer Success, Finance, and Product, and includes a measurement layer that connects execution to board-level reporting.

This structure helps ensure that the 100-Day Plan is not a one-time effort, but the start of a predictable system for commercial growth.

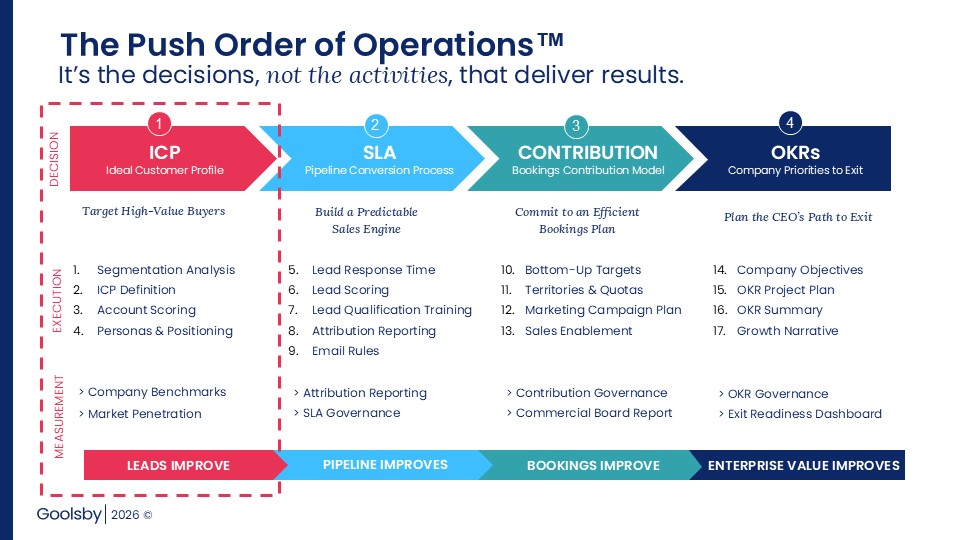

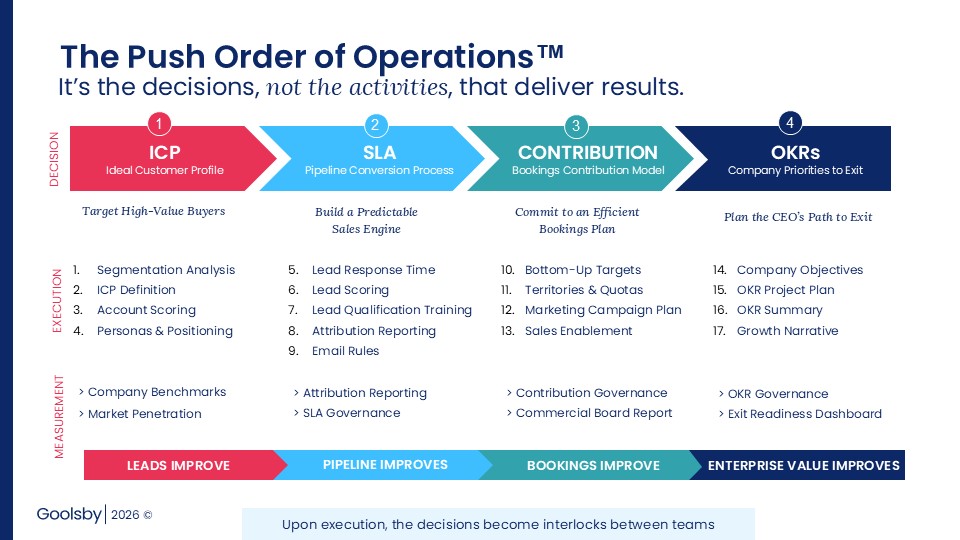

The Push Order of Operations: The CEO’s Decision Sequence

The Push Order of Operations is a four-decision framework that sequences commercial execution for PE-backed SaaS companies. It is designed to help ensure execution compounds rather than fragments.

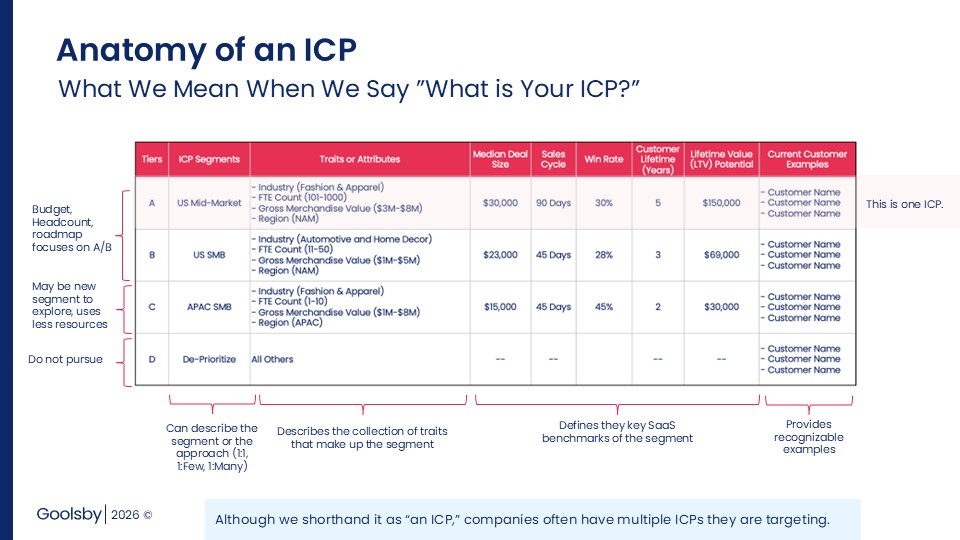

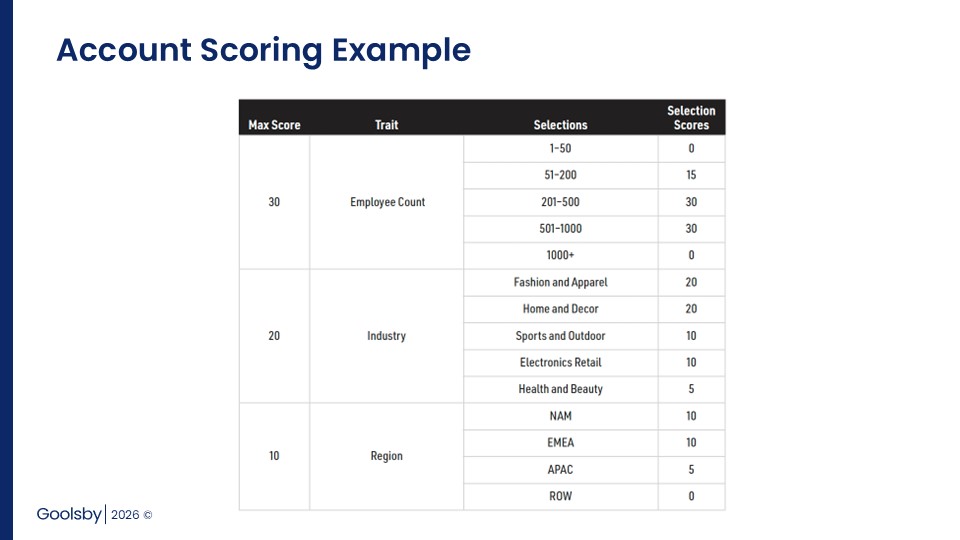

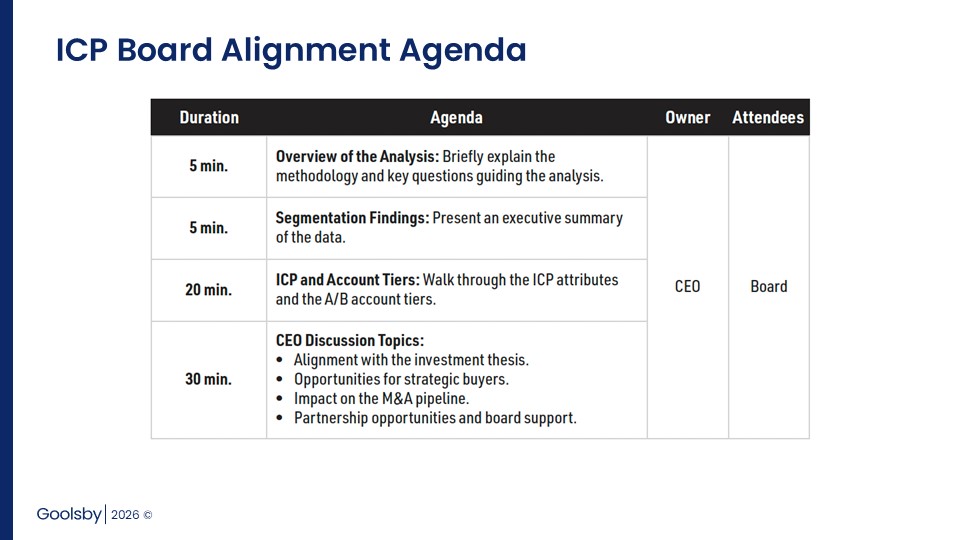

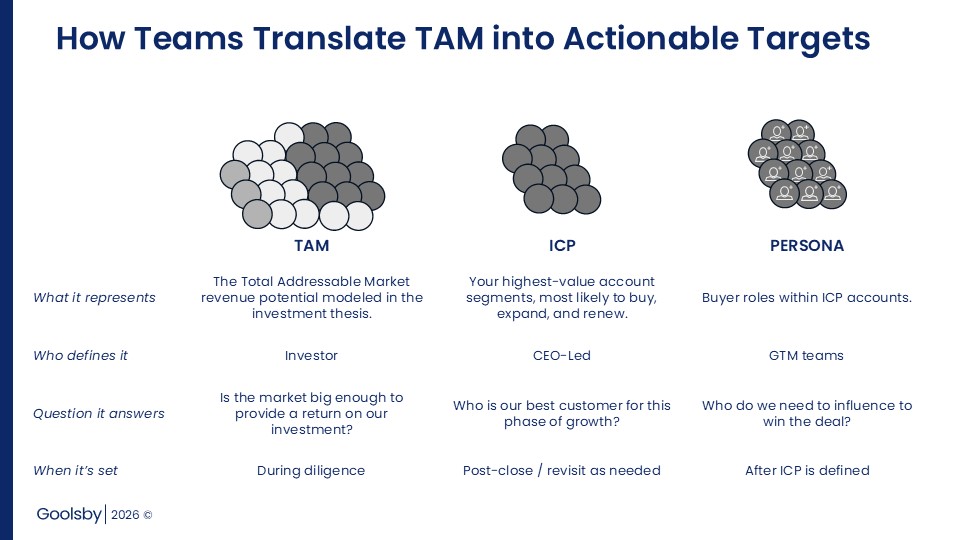

Decision 1: The ICP Decision — Who do we target?

The Ideal Customer Profile Decision defines which accounts have the highest propensity to buy, renew, and expand. This is not a marketing exercise. It is a strategic decision that informs territory design, quota setting, pipeline targets, campaign investment, and product roadmap priorities. In a PE context, the ICP is validated against the investment thesis, extending beyond historical pattern recognition.

Decision 2: The SLA Decision — How do we convert?

The Pipeline Conversion Process defines how marketing, sales, and RevOps coordinate to move leads through the funnel. It establishes lead response times, scoring rules, qualification criteria, attribution reporting, and email rules. Without The Push-Style SLA, every function optimizes independently. With one, you build a coordinated sales engine.

Decision 3: The Contribution Decision — Where do bookings come from?

The Bookings Contribution Model is often a missing layer. It connects the financial plan to commercial execution. It defines how the bookings number will be sourced by channel, by segment, by rep and what pipeline coverage is required to hit plan. This model turns a revenue target into an operational commitment that each function can own.

Decision 4: The OKR Decision — What does the CEO prioritize over the long-term?

The OKR Decision maps Objectives and Key Results back to value creation levers and exit targets. Unlike generic OKR templates, the Push OKR Framework uses the investment thesis, Value Creation Plan, and exit targets as the starting point. This ensures company-wide priorities align directly with what the investor needs to see at exit.

The sequencing is what sets the Push Framework apart from traditional GTM plans.. Each decision creates the inputs required for the next. The ICP defines who to target. The SLA defines how those targets convert into pipeline. The Contribution Model defines where we will invest to source more of the pipeline that turns into bookings. The OKRs connects all of this execution to long-term exit outcomes.

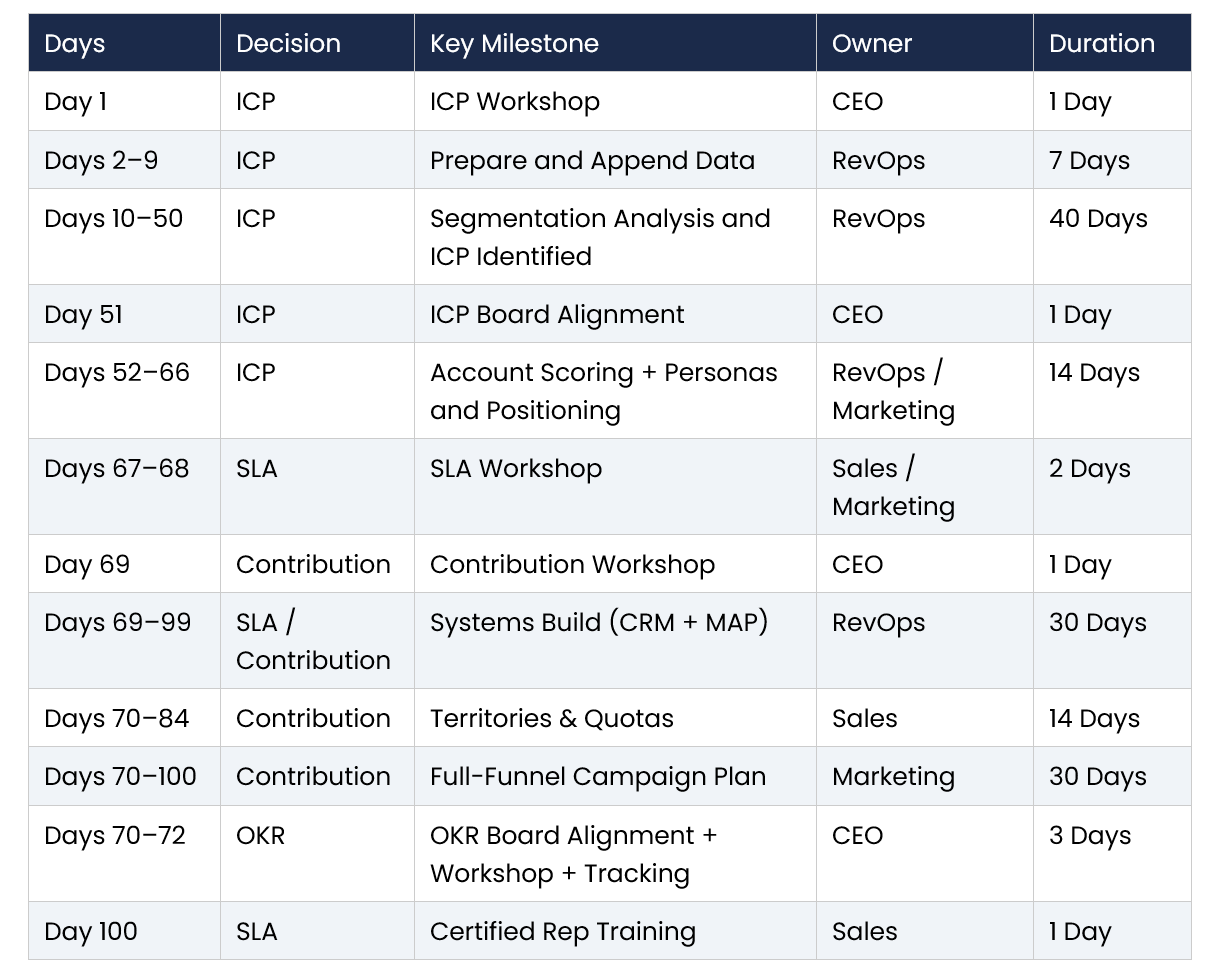

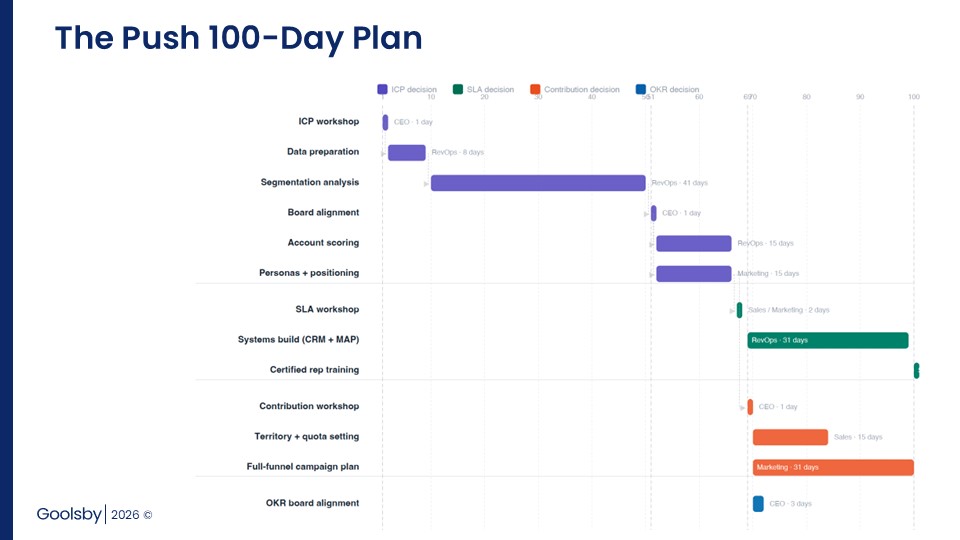

The 100-Day Execution Timeline

The following outlines the execution timeline. This is not a conceptual framework, it is a sequenced plan with defined milestones, owners, and durations.

Notice the parallel structure of execution. After the ICP is defined on Day 51, multiple workstreams begin to run simultaneously. Account scoring and persona development proceed alongside SLA preparation, while the Contribution Workshop, territory planning, campaign planning, and OKR work overlap.

This structure is intentional. The ICP decision enables downstream execution, and once it is established, execution velocity increases.

The Push 100-Day Plan: How the four growth decisions sequence across parallel workstreams. Each decision creates the inputs required for the next.

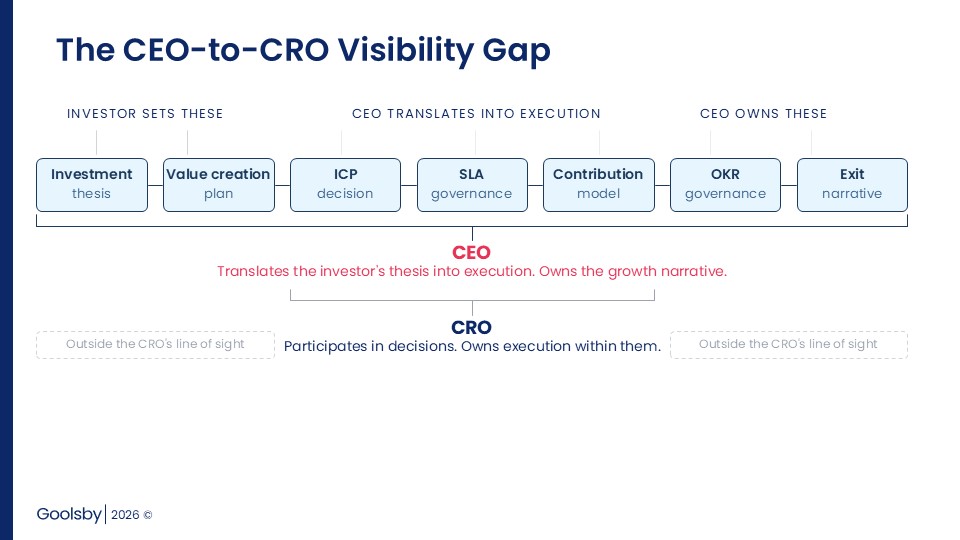

Why Delegating Commercial Strategy to the CRO Fails

In a PE-backed SaaS company, commercial strategy is most effective when owned by the CEO. The CEO is the only role with both the authority and full-system visibility to coordinate execution across functions and align it to the investment thesis.

When that responsibility is delegated to the CRO, strategy can become functionally optimized rather than systemically aligned. Over time, this creates execution risk and makes it more difficult to present a coherent growth narrative to the board.

When commercial strategy is not clearly owned by the CEO, three issues can emerge:

- The Board Hears Two Narratives

The CEO presents direction. The CRO reports on pipeline. Without a clear connection between the two, the board lacks a cohesive view of progress, which can lead to increased scrutiny.

- The CEO Loses the Growth Story

When the CEO is not shaping commercial strategy, it becomes harder to explain performance and priorities. Over time, the CEO can appear less able to control commercial results. - Execution Fragments Across Functions

Without clear authority to drive company-wide coordination, functions tend to optimize in silos. Decisions may make sense in isolation, but the system becomes less aligned and less predictable.

The CEO does not need to manage day-to-day pipeline activity, but should maintain ownership of how the system fits together and how decisions connect across functions to deliver the investment thesis.

This is a CEO-led commercial model where the CEO owns commercial direction, and the CRO owns execution against that direction. The CRO executes within the system; the CEO ensures the system is aligned to the growth thesis.

This is not work the CRO can do alone.

What Operating Partners Look for in the First 90 Days

The first 90 days of the investment serve as an early signal of how a CEO will operate under PE ownership. During this period, the CEO is not only leading the team through the core growth decisions, but also demonstrating to investors how execution will be managed going forward.

In practice, operating partners tend to look for three things:

- Acting with urgency

Progress against gaps identified during diligence should be visible early. This includes establishing scalable processes, addressing execution risks, and demonstrating forward momentum. The signal is not speed alone, but the ability to prioritize and move with intent. - Demonstrating operational control

The CEO should show ownership of the core growth decisions and how they translate into execution. This includes visibility into key metrics, clarity in decision-making, and consistency in how systems are built and managed. The focus is less on perfection and more on whether the business is becoming more structured and predictable. - Building investor confidence through execution

Operating partners look for a clear connection between the investment thesis and day-to-day execution. This includes grounding decisions in data, communicating tradeoffs clearly, and showing how current actions map to the Value Creation Plan and long-term outcomes.

Consistent performance across these areas helps establish credibility with the board and creates greater flexibility as the business scales.

Frequently Asked Questions

What if I am not new to the CEO role?

The Push Framework applies whether you are in your first 100 days or several years into the role. If you do not yet have a structured ICP, SLA, contribution model, and OKR framework—or are experiencing a mid-hold slowdown or decline, the 100-Day Plan provides a sequence to build or reset them. The timeline may compress depending on what is already in place.

How does this apply to founder-CEOs who took PE investment?

Founder-CEOs often face a different version of this challenge. You know the business well, but may not have operated within this phase of growth with the level of transparency and structure investors expect. The Push Framework does not replace instinct. It provides structure, measurement, and governance to support it.

What if my board has already set the strategy?

In that case, the focus shifts to whether the strategy has been translated into a commercial execution plan with clear sequencing, ownership, and measurable milestones. Without that translation, execution can remain unclear. The 100-Day Plan is designed to bridge that gap.

How do I handle a CRO who resists this structure?

This is often a framing issue. The intent is not to reduce the CRO’s authority, but to provide clearer direction. The CRO executes the commercial strategy, while the CEO ensures it is defined and aligned to broader business objectives. Resistance often reflects a lack of prior alignment rather than a structural issue.

What if I am an operating partner evaluating a CEO?

A practical approach is to ask the CEO to walk through their ICP, pipeline conversion process, where incremental investment would drive growth, and their top company priorities. Clarity in these areas is a useful signal of execution maturity. Where gaps exist, a structured diagnostic (such as the Push Commercial Audit) can help identify them within a few weeks.

What does this look like for a $20M–$200M ARR company specifically?

The framework scales across this range, but execution expectations evolve. At lower ARR levels, ICP definitions may be less detailed. At higher levels, contribution modeling and cross-functional coordination typically become more complex. The decision sequence remains consistent, even as execution complexity increases.

How does the Push framework differ from a standard GTM plan?

A GTM plan is typically organized as a set of initiatives by function. The Push Framework organizes execution around a sequence of decisions and outcomes. In practice, this helps clarify not just what teams should do, but how decisions connect across functions and build on one another over time.

Glossary

- 100-Day Plan:

A structured execution plan that sequences the initial phase of commercial and operational activities following investment. Includes defined milestones, owners, durations, and dependencies to align the organization and establish early momentum. - Contribution Decision:

The third decision. Builds the bookings contribution model that defines how the revenue target will be sourced by channel, segment, and rep with required pipeline coverage. - Exit Readiness:

The state of organizational maturity across metrics, processes, governance, and narrative that determines whether a company can withstand buyer diligence and command a premium valuation. - Exit Targets:

Defined performance benchmarks tied to the growth thesis and Value Creation Plan, used to track progress toward the desired exit outcome. Typically measured quarterly and used by investors to assess whether the company is on track to achieve its return objectives. - Growth Narrative:

The CEO’s ability to connect current commercial results to forward-looking performance and enterprise value creation in a single, coherent story told to the board. - Growth Thesis:

The investment hypothesis that defines how a company is expected to increase revenue and enterprise value over the hold period. Typically includes target segments, growth levers, and operational improvements, and serves as the basis for evaluating performance. - Hold Period:

The time frame a private equity firm expects to own and grow a company before exiting, typically 3–7 years. All growth planning, execution milestones, and exit targets are structured within this window. - IC Memo (Investment Committee Memorandum):

The document a PE investor uses to get deal approval from their investment committee. Contains the investment thesis, growth assumptions, and return expectations. - ICP Decision:

The first decision in the Push framework. Defines which accounts have the highest propensity to buy, renew, and expand based on segmentation analysis validated against the investment thesis. - OKR Decision:

The fourth decision. Maps Objectives and Key Results to value creation levers and exit targets, aligning company-wide execution with investor expectations. - Pipeline Conversion Process (SLA):

A defined agreement between Marketing, Sales, and RevOps that governs how leads move through the funnel. Includes response times, qualification criteria, routing rules, and conversion expectations to ensure coordinated execution. - Push Order of Operations:

A four-decision framework (ICP, SLA, Contribution, OKRs) that sequences commercial execution for PE-backed SaaS companies. Each decision creates the inputs the next one requires. - SLA Decision:

The second decision. Establishes the pipeline conversion process: how Marketing, Sales, and RevOps coordinate to move leads through the funnel with defined rules, timing, and accountability. - Value Creation Plan (VCP):

The execution roadmap that connects investor expectations to operational milestones. Defines the growth levers that must be pulled during the hold period to drive enterprise value.

Next Step: The Push Commercial Audit

The Push Commercial Audit identifies growth levers and execution risks across the commercial organization within two to four weeks. It maps symptoms to root causes and provides a prioritized execution roadmap.

For CEOs in their first 100 days, it helps clarify where to focus. For operating partners, it provides a structured assessment of commercial execution maturity across the portfolio.

February 26, 2026